Managing a Community Reinvestment Act (CRA) program can be complex, especially when balancing the various demands of financial institutions. For CRA practitioners, understanding how community development (CD) services and volunteerism contribute to CRA credit is essential for maximizing the impact of their efforts. Community development services can range from traditional banking activities to leveraging the expertise of bank employees in areas such as human resources, IT, legal, and compliance to support nonprofits serving low- and moderate-income populations. With a better understanding of what qualifies as a community development service, financial institutions can strengthen their CRA strategies and contribute more effectively to their communities.

You can probably recite the community development “hooks” in your sleep. If, however, you are new to CRA, print this out and keep it handy!

What Qualifies As A Community Development Service

At its core, a CRA-qualified service must meet the following criteria:

-

Have a primary purpose of community development

-

Be related to the provision of financial services

-

Be performed on behalf of the bank

-

Not have been considered in the evaluation of the bank’s retail banking services

-

Benefit the bank’s assessment area or a broader statewide or regional area that includes the bank’s assessment area

When preparing for a CRA exam, it’s important to understand how your institution’s community development services will be evaluated. The exam will focus on several key areas, and here’s what you will need to do so you’re fully prepared:

Identify Community Development Services

Your exam will begin by identifying the community development services your bank provides, including services through affiliates if applicable. Be sure to have discussions with your management team and review available materials to confirm the following:

-

Whether these services have been considered under the lending or investments tests.

-

If any services are provided by affiliates, ensure that they are not also claimed by other affiliated institutions to avoid double-counting.

Evaluate Service Impact and Innovation

The exam will also assess the extent to which your community development services meet community needs and align with your bank's capacity. Specifically, the exam will look at:

-

Where services are provided: Are they in your bank’s assessment area, or do they extend to a broader region that includes areas you serve?

-

Innovativeness: Are your services offering new ways to support low- or moderate-income individuals or communities? Do they address gaps in service or reach underserved populations?

-

Community focus: How well do your services address the needs of low- or moderate-income individuals or communities? Are you responsive to available opportunities for community development?

The CRA Interagency Q&A document released in 2016 expanded the definition of "provision of financial services" to include non-traditional roles such as compliance, risk management, and project management. This broadening of the definition allows banks to leverage a wider range of expertise to support community organizations like Community Development Financial Institutions (CDFIs) or social service nonprofits. For example, a bank employee from the loan servicing division could volunteer to help a CDFI establish efficient loan servicing processes, or an employee from vendor management could assist a nonprofit in managing risks tied to a large government contract. These services not only help nonprofits operate more effectively but also provide valuable opportunities for banks to contribute to community development without incurring significant financial costs.

Community Development Service Ideas

There are many ways for your institution to earn CD service hours. Just make sure that the service hours meet the criteria outlined above and are properly documented.

Here are a few ways your institution might earn CD service hours:

Volunteer with the VITA Program

Banks can play a pivotal role in supporting community development through various services and partnerships. One underutilized option is participation in the Volunteer Income Tax Assistance (VITA) program. Administered by the IRS, VITA and its companion program, Tax Counseling for the Elderly (TCE), provide free basic tax return preparation for eligible individuals. This program has been in operation for over 50 years and is designed to assist:

-

Individuals with an annual income of $67,000 or less

-

Persons with disabilities

-

Taxpayers with limited English proficiency

Bank employees can become trained volunteers to offer tax assistance to low- and moderate-income families in their communities. By participating, employees contribute to the preparation of millions of tax returns annually at tax sites nationwide. Additionally, the time spent receiving certification and preparing taxes can count toward Community Reinvestment Act (CRA) credit.

See why this banker spent 16 hours a week filing taxes (and how he gets CRA credit for it).

Partner with the Federal Home Loan Bank

Another valuable opportunity comes through the Federal Home Loan Bank (FHLB), which offers a range of programs and partnership opportunities that can help your bank earn CRA credit. Partnering with your local FHLB can provide access to a variety of products and services that might be more difficult to implement independently.

Work with a Community Development Financial Institution

Moreover, engaging with Community Development Financial Institutions (CDFIs) in your area can offer further avenues for community support. While partnerships with CDFIs are often focused on deploying loans or capital, there are also numerous service-based opportunities. These can include assisting with loan underwriting, joining their board, or collaborating on the development of new products, services, and marketing strategies.

By exploring these options, your bank can enhance its community development efforts and potentially earn valuable CRA credit while making a meaningful impact.

Read this article to learn more about the benefits of partnering with a CDFI. And read this article for ideas on how to partner with a CDFI.

How to Properly Document Community Development (CD) Service Hours

Documenting your CD services in meticulous detail is essential to ensure that your bank receives full CRA credit. This process isn’t just about keeping records—it’s about telling your institution's community impact story.

Here’s how to properly document your CD Service Hours:

Capture All Relevant Details

Make sure to capture all relevant data points, including:

-

Organization Details: Include the organization’s mission, website, and any documents that explain its purpose

-

Location Information: Include the assessment area(s) benefitted and where the service took place (automatic goecoding is a big plus!)

-

CD Purpose: Clearly show how the activity aligns with CRA objectives and which “hook” it falls under (affordable housing, community services, economic development, or revitalization/stabilization)

Demonstrate Impact

Now it’s time to go beyond the hours served. Make sure to clearly explain how the service contributed to the overall economic improvement of the target community. Ask yourself these questions:

-

Did it help a nonprofit expand its services?

-

Was there measurable improvement in financial education or economic conditions for LMI individuals?

-

How does this align with broader community needs?

Provide Supporting Evidence

It’s important to not only say how each service hours impacts your community, but also to show it with supporting documentation.

During a CRA exam, be ready to back up your services with:

-

Time logs and volunteer reports

-

Photos or testimonials from events

-

Documentation of the nonprofit’s feedback and how it benefited from your support

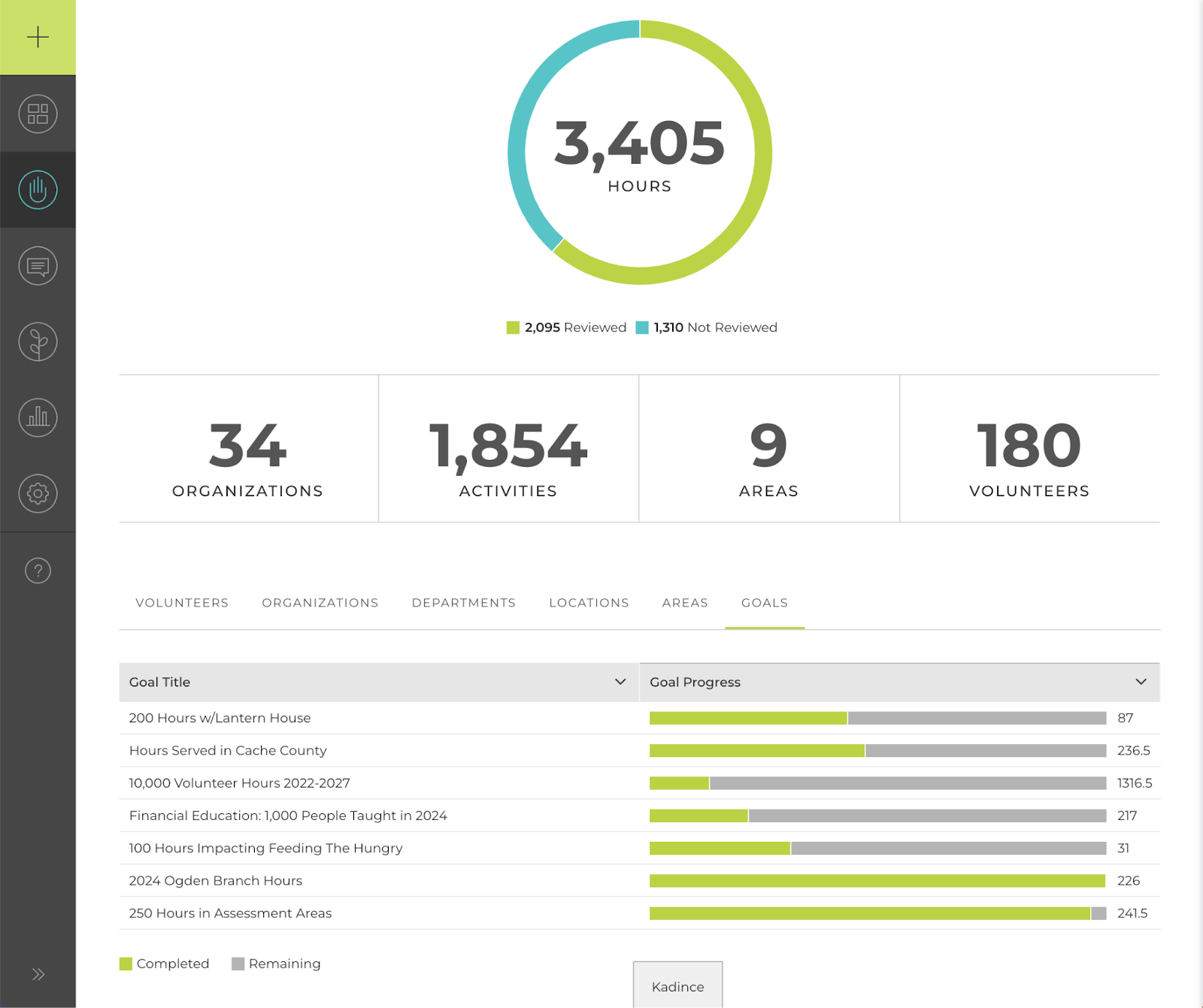

Leverage Tools That Track This Data

Does that sound a bit overwhelming? Don’t worry, there are lots of different tools and softwares you might use to properly document CD services and other CRA-related data.

For example, Kadince software makes it easy to track, manage, and report your institution’s CD services. With Kadince, you can:

-

Use web-based forms to collect service hours with ease

-

Attach supporting documents to each record, accessible with a single click

-

Automate CRA review tasks with Kadince workflows

-

Automatically geocode submissions to track impact across markets, counties, and assessment areas, with tract and demographic details auto-populated

To learn more about Kadince and see how it properly track CD services and more, schedule a 30-minute demo.

If your institution doesn’t use software designed to track CD services, then make sure you have a strict process and clear guideline document so everyone is on the same page.

The Bottom Line

By understanding the fundamentals of CRA community development services and volunteerism, financial institutions can make the most of their employees' skills to support their local communities. Time spent volunteering is a cost-effective way to earn CRA credit, and when employees offer their expertise in areas such as compliance or project management, it can help nonprofit organizations thrive. The key is ensuring that the services provided meet the CRA’s criteria and are appropriately documented. In doing so, banks can strengthen their CRA performance while also fostering positive, long-term economic development in underserved areas.

To learn more about CRA service hours, check out CRA Today. With CRA training, professional development, and certification, CRA Today has something for everyone.

And if you're new to the CRA, read this article for beginners. It covers everything you need to know to get started.

And for ideas on spending less time reviewing service hours for CRA eligibility, check out this article.

*This article was updated on January 17, 2025 to better explain service hours and the how to document them.

None of Kadince, Inc., its affiliates, or its respective employees, directors, officers, and agents (collectively, “Kadince”) are responsible or liable for any content or information incorporated herein. Read full disclosure.