Want to boost your bank's CDFI partnerships? Download this CDFI partnership implementation checklist.

Struggling to find ways to bring affordable, flexible capital into your community while creating net income for your bank? A partnership with a Community Development Financial Institution (CDFI) might be the answer you’re looking for!

As you know, your bank is constrained to ensure that you make safe and sound loans that meet your underwriting and regulatory requirements. Sometimes these restrictions prevent you from making smaller loans and loans that push your underwriting and regulatory boundaries. This is where CDFIs come into the picture.

CDFIs are often nonprofit organizations that don’t have the same regulatory oversight and restrictions; therefore, they can provide more flexible funding than traditional financial institutions. They also pair their loans with technical assistance, which creates a powerful combination to serve those who don’t typically have access to credit. Investments and partnerships with CDFIs can then help you reinvest your capital and resources into the community in creative ways that may generate income (interest income and maintain deposits) and earn CRA credit for your bank.

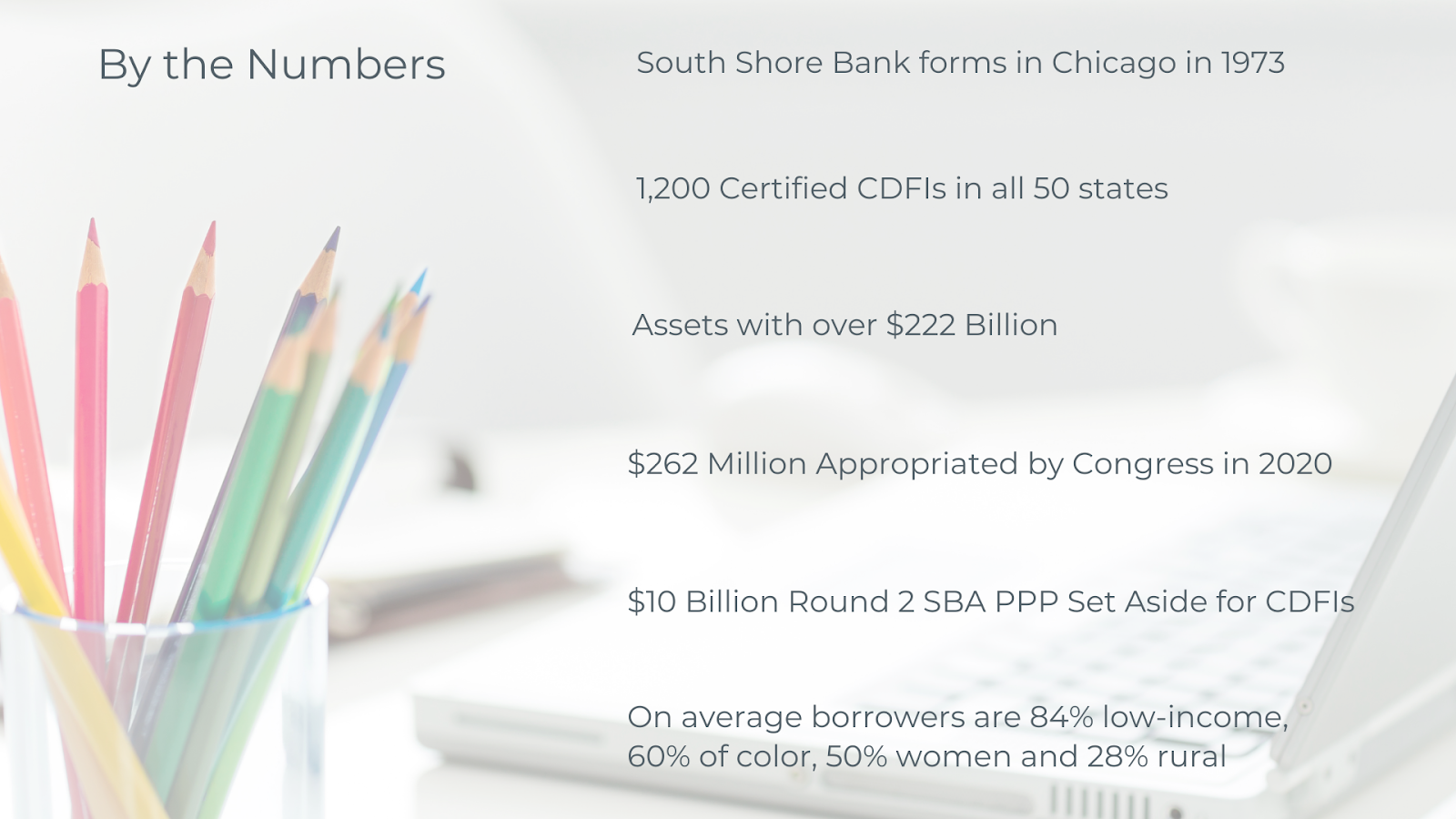

CDFIs are financial institutions that have a primary mission of community development and have been certified by the CDFI Fund. They can be banks, credit unions, loan funds, or venture capital funds. CDFIs have a long, rich history of supporting low-income communities across the country. Today they are better understood than ever before and are being recognized for the great impact they can have. Billions of dollars are cycling through these innovative financing entities. Click here for an infographic summary of CDFIs.

CDFIs foster economic opportunities and revitalize neighborhoods. They help families finance their first homes, support local businesses, and invest in local health centers, schools, or community centers. There is power in leveraging your program to support the CDFI movement, and there are numerous opportunities for you to get involved.

How to Support CDFIs

Later in this series, we'll highlight the various ways banks can partner with CDFIs. To highlight the first level of support, we have to mention capital. CDFIs need affordable capital, but that doesn’t have to mean grants. For example, consider how your bank can use Equity Equivalent Investments (EQ2s) or loan pools to bring lower-cost microloans into your community.

Equity Equivalent Investments are the most flexible and powerful investment you can provide to a CDFI. They are long-term, fully subordinated debt instruments with features, such as rolling terms, that allow them to function like equity. EQ2s make it easier for CDFIs to offer more responsive financing products with longer loan terms.

Often, banks are unable to make large loans to a CDFI on their own. Loan pools bring two or more financial institutions together to make a loan to a CDFI that is larger than either institution is comfortable with on their own. The funds can be organized as a lending consortium in which the participating banks pool their funds as investments in a consortium.

Capital investments are numerous, varied, and can come in the form of stock purchase, ownership interest, and grants. There’s a CDFI investment opportunity out there to fit your bank’s portfolio while supporting your CRA goals!

Where To Start

Before investing in a CDFI, you might want to get to know one or more in your community. Look for opportunities to provide your services to your local CDFIs. CDFIs can benefit from:

- Loan servicing arrangements

- Traditional banking services

- Volunteers for their technical assistance and training programs

You can leverage your bank’s core business with CDFI resources to produce a powerful difference in meeting the credit needs of those who are underserved in your local communities. Use this leverage and opportunity to reach minority neighborhoods and micro-businesses.

Check out the Opportunity Finance Network’s interactive map to find a CDFI in your community today! And if your institution is interested in becoming a certified CDFI, click here for more information.

To learn more about how to partner with a CDFI, check out this article and download this high-level checklist.

Check out our webinars page for more in-depth CRA trainings.

None of Kadince, Inc., its affiliates, or its respective employees, directors, officers, and agents (collectively, “Kadince”) are responsible or liable for any content or information incorporated herein. Read full disclosure.

By: Linda Ezuka | May 31, 2021