As a Small bank employee, you juggle a lot of responsibilities. Chances are you’re the only CRA/compliance person at the bank, and even if you’re not, you likely don’t have all the resources you need.

Keeping your bank compliant under the Community Reinvestment Act (CRA) is a big task, but all the resources out there seem to be aimed at larger institutions. The needs of a $15B bank just aren’t the same for a small bank.

Let’s change that.

This article covers what Small banks need to know about the Community Reinvestment Act.

(For the purposes of this article, a “Small bank” is considered a bank with less than $391 million in assets as of the last two calendar years. This matches the current Small bank definition provided by the Federal Financial Institutions Examination Council, or FFIEC.)

What is the Community Reinvestment Act?

Let’s start simple, shall we? The Community Reinvestment Act is BIG, and we can’t cover every aspect of it in a blog article like this.

The Community Reinvestment Act was created in 1977 to prevent banks from “redlining” community members, or refusing to lend to them based on race or where they lived. Bankers saw these low-to-moderate income individuals as too risky, and they weren’t giving the financial support community members needed.

Now banks must go through a CRA exam every 3 or so years to ensure that they are meeting the credit needs of their communities. After each CRA exam, the bank is given a rating based on how well they’ve done. There are four CRA ratings:

-

Substantial Noncompliance

-

Needs to Improve

-

Satisfactory

-

Outstanding

This rating is public, so anyone can look up their bank and see how it’s helping the community. Understandably, banks want to score well.

CRA exams for Small banks

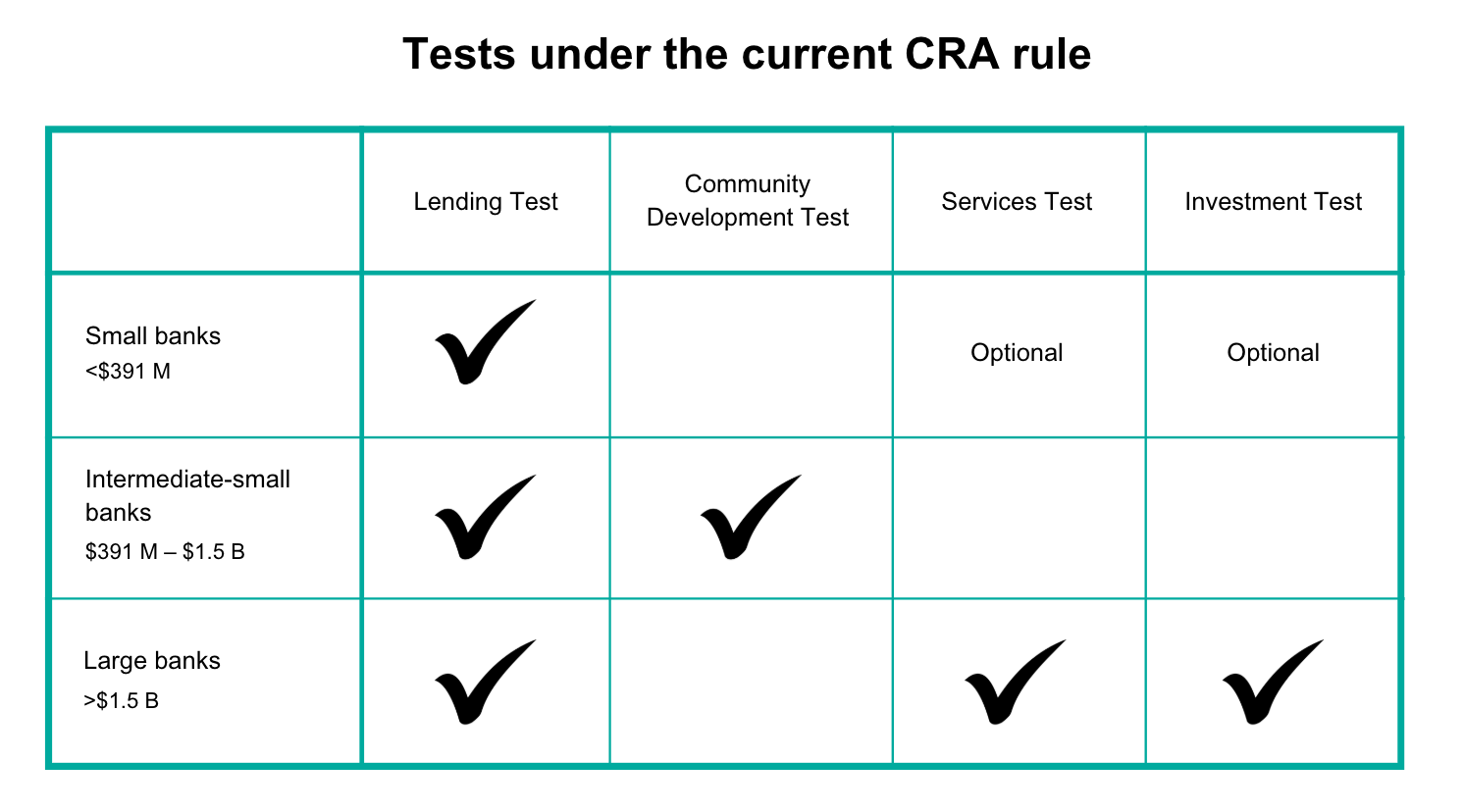

A bank’s asset size determines which test(s) it must go through during the CRA exam and how much data has to be tracked. Currently, there are three asset tiers: Small, Intermediate-Small, and Large. As we’ll discuss later in the article, these size names and their asset tiers are likely to change within the next few years.

Every year, bank sizes are reassessed and requirements potentially changed. Imagine finally getting the hang of things and then jumping an asset tier. So much work!

Here are the current asset tiers:

-

Small—assets of less than $391 million (as of December 31 of either of the prior two calendar years)

-

Intermediate-Small—assets between $391 million and $1.503 billion

-

Large—assets above $1.503 billion

There are four separate tests to a CRA exam, and a bank’s asset size determines which test(s) they must complete.

-

Lending Test

-

Community Development Test

-

Services Test

-

Investment Test

While Intermediate-Small and Large banks are subject to 2 or 3 tests each, Small banks only have to worry about the Lending Test. Small banks can also choose to go through the Services and Investments Tests. These tests are optional, and there are various reasons a Small bank might choose to participate, including chasing a better CRA rating, preparing for eventual growth, and meeting strategic objectives.

Overall, the CRA exam is less burdensome for Small banks than it is for Intermediate-Small or Large ones. By focusing solely on the Lending Test, small banks can make up for their limited resources and capabilities while shining a bright light on their strong lending activities.

The Lending Test for Small banks

The Lending Test is the only test a Small bank is required to complete. Just like it sounds, this test is all about the bank’s lending performance. Specifically, this test examines a bank’s applicable home mortgage loans, small business loans, and small farm loans.

Here are some terms you should know:

-

Assessment Area(s)—The geographic region(s) where a bank’s CRA performance is evaluated, typically where the bank has branches, ATMs, or deposit-taking facilities, and where it conducts a substantial portion of its lending activities

-

Geographic distribution—How loans are distributed across different geographic areas (low-, moderate-, middle- and upper-income) within the bank’s assessment areas.

-

Borrower distribution—An umbrella term referring to income distribution and revenue distribution metrics

-

Income distribution—How home mortgage loans are distributed among different income levels within the bank’s assessment areas

-

Revenue distribution—How commercial loans are distributed among different revenue levels within the bank’s assessment areas

-

Inside/Outside AA distribution—The amount (# and $) of loans made by the bank within its assessment areas vs outside

-

Loan-to-deposit ratio—The ratio of the bank's loans to its deposits, indicating how much of the deposits are used for lending within the community

-

Performance context—The specific economic, demographic, competitive landscape, and institutional factors that influence a bank's ability to meet the credit needs of its community

-

Home Mortgage Loans—Loans of any amount made to individuals or families that fall under the categories of home purchase loans, home improvement loans, and refinancing loans. These loans must be secured by residential real estate

-

Small Business Loans—Loans under $1 million made to businesses with gross annual revenues of $1 million or less (call report codes 1e1, 1e2, or 4a.)

-

Small Farm Loans—Loans under $500,000 made to agricultural businesses with gross annual revenues of $1 million or less (call report codes 1b or 3)

Basically, a CRA Officer or compliance professional analyzes all of the bank’s applicable loans while keeping an eye on their geographical distribution, borrower distribution, and inside/outside AA distribution. The CRA Officer presents these analytics to their CRA examiner and crosses their fingers that the examiner considers them favorably.

If a bank has made enough qualified loans to effectively serve the credit needs of its assessment areas (although there’s no magic number), then it should score a Satisfactory or even Outstanding rating. Yes, this is rather subjective, and it ultimately falls on the CRA examiner to decide how well the bank met the credit needs of its assessment areas, given the performance context. That’s part of the reason the Community Reinvestment Act is so confusing!

A note on Assessment Areas (AAs)

Choosing your bank’s Assessment Area(s) can be daunting. You need to choose the correct AAs, and you don’t want too few or too many.

Generally speaking, your Assessment Areas should be chosen based on the locations of your main branch, additional branches, and deposit-taking ATMs. Just be sure not to exclude low- and moderate-income (LMI) areas, as this could raise red flags with regulators. For many Small banks, one or two Assessment Areas work well. But each bank is different, and it’s up to you and your team to delineate AAs and properly track any loans given.

Here are some questions to consider when choosing your Assessment Areas:

-

Where do you naturally lend given your branching and retail network?

-

Will you be expanding or contracting your retail delivery system in the near term?

-

What is executive management's strategic vision for future growth?

-

Where do you uniquely serve (niches)?

-

Are your Assessment Areas too broad or narrow? An overly broad AA might dilute the bank’s ability to effectively meet credit needs, while a too narrow AA could limit opportunities to demonstrate strong performance.

Your Assessment Areas are not written in stone. In fact, you should regularly review and (when necessary) update your AAs to reflect changes in the bank’s business strategy, expansion of services, or shifts in local demographics.

How Small banks manage CRA data

Believe it or not, most Small banks use spreadsheets or even binders to analyze their bank’s lending performance. While this works for some Small banks that don’t process many loans, this method is typically manual and time-consuming.

Instead, you can use Kadince software to track all the data you need for your Lending Test. All your loans are kept in one place, so no more switching between various spreadsheets and tracking down emails, files, or even worse, 3-ring binders. You can even build examiner-style reports or give your CRA examiner read-only access to the data you want them to see with all the supporting documents tied to each loan.

Here’s a sneak peek at the Kadince loan dashboard. If you want to learn more, schedule a 30-minute demo. We promise not to go all salesy on you.

The CRA exam process for Small banks

Before the exam

There’s a lot of work that goes into preparing for a CRA exam. Most of this work falls on the CRA Officer or a small team of CRA professionals. Since you’re part of a Small bank, it’s probably just you…

Before the CRA exam, the CRA Officer or another member of the CRA team has to:

-

Create a CRA strategy and action plan (optional, but helpful)

-

Conduct a CRA self-assessment to see where the CRA program is (also optional, but VERY helpful)

-

Collect and manage all the necessary data

-

Gather all supporting documentation and build reports for CRA examiners

Preparing for a CRA exam takes a lot of time, but at least you only have to go through the Lending Test, right?

During the exam

Whether the exam is on-site or online, the CRA Officer will likely be very involved in the process. From weekly chats with examiners to defending the bank’s CRA performance, the CRA Officer has quite a busy time. If an exam is on-site, the CRA Officer may even be responsible for reserving private conference rooms, coordinating parking and building access, and finding local menus to support lunch breaks. Some CRA Officers assign an exam liaison to ensure a smooth exam.

After the exam

Once the exam is over, CRA Officers immediately start preparing for the next one (after a much needed vacation or some PTO, of course).

To begin, you’ll examine your results. Whether you achieved a Satisfactory, Needs to Improve, or Outstanding rating, there’s always something to improve the next time around. Now is the time to reflect on your program’s performance and build a plan for the future.

If you have any questions about your rating or why you didn’t get credit for that small farm loan, you can reach out to your examiner and ask. Having a good relationship with your examiner is a critical part of building a lasting CRA program.

You should also revisit your CRA strategy, action plan, and self-assessment. Chances are your executive team or board of directors will want a report, and it’s a good idea to share these documents with them and pitch your plan for the future.

Regulatory change is coming

For the first time since 1977, the Community Reinvestment Act is getting a major update. This update is meant to modernize and strengthen the CRA framework, plus provide more direction on what does and doesn’t qualify for credit.

While this update was originally meant to take effect in 2026, it has since been put on pause. There are a few outstanding lawsuits that need to be resolved, so we don’t yet know exactly when (or if) these changes will take effect.

Here are some key changes coming to the CRA that affect Small banks (if the new rule is implemented as is):

New Asset Sizes

Under the current CRA regulations, any bank with less than $391 million in assets is considered Small.

Here’s the breakdown under the new rule:

-

Small—assets of less than $600 million

-

Intermediate—assets between $600 million and $2 billion

-

Large—assets $2 billion or more (with banks over $10 billion in assets being subject to further requirements)

This means that many banks currently considered Intermediate-Small may soon be Small, and therefore will only have to complete the Lending Test, or the Retail Lending Test as explained below.

Retail Lending Test

Under the new rule, Small banks can choose to either complete the Lending Test as it is currently organized or opt into a new Retail Lending Test.

This Retail Lending Test isn’t very different from the current Lending Test, but would analyze your Small bank’s retail lending, including applicable home mortgage loans, multi-family loans, small business loans, small farm loans, and automobile loans.

If your bank offers a significant amount of multi-family or automobile loans, and you believe you may want to opt into this test when it takes effect, you should start preparing to track this extra data now.

In fact, each of the four tests is getting a bit of an overhaul, although Small banks are still only required to complete one. The four tests may soon be:

-

Retail Lending Test

-

Retail Services and Products Test

-

Community Development Financing Test

-

Community Development Services Test

We won’t go into each of these tests and what they mean in this article. Just know that as a Small bank, you only need to worry about whether you’re going to stick with the current Lending Test or try your hand at the Retail Lending Test.

Public File Updates

Under the new rule, any bank with a public-facing website must publish a Public File annually. This file must be up-to-date and easily accessible on their website. Here is everything your Small bank’s Public File needs to have under the new rule (bolded items must be updated quarterly instead of annually):

-

List of your Assessment Areas

-

Maps of your AAs

-

Branch locations

-

Product and service offerings

-

Disclosure statement that tells where to find your HMDA data on the CFPB website

-

Last two years of your bank’s small business and small farm disclosure statements (found on the FFIEC website)

-

Public section of your bank’s most recent Performance Evaluation

-

The bank’s loan-to-deposit ratio for each quarter of the prior calendar year

-

The bank’s strategic plan (if applicable)

-

Information on your lending, investments, and services (If you opt-in to the Investment or Service Tests)

-

Written comments received from the public for the current year

- List of branches opened or closed during the current year

- Current efforts to improve the bank’s CRA performance (only for banks who received a less than Satisfactory rating)

You can present your Public File however you’d like. Most banks create multiple documents that include all of the above information and have a section on their website specifically dedicated to their Public File.

To get an idea of how the CRA might look under the new rules, download this free Regulatory Change Preparation Guide for Small Banks. This guide will help you prepare for the new CRA rule and formulate a plan while keeping key risks in mind.

Download the Regulatory Change Preparation Guide

—

There you have it! You just learned what Small banks need to know about the Community Reinvestment Act, and it wasn’t as bad as you thought, was it?

To learn more about how Small banks should prepare for the CRA (especially when it comes to the new rule), watch this free recorded webinar presented by CRA expert Linda Ezuka of CRA Today.

None of Kadince, Inc., its affiliates, or its respective employees, directors, officers, and agents (collectively, “Kadince”) are responsible or liable for any content or information incorporated herein. Read full disclosure.