Are you ready for your next CRA exam? If you’re like most CRA professionals, preparing for a CRA exam is a never-ending process. One way to make this process a little more manageable is by creating a CRA self-assessment. Most CRA officers find that once they create a CRA self-assessment and commit to keeping it up to date, it can be a powerful tool to ensure a smooth exam experience for all stakeholders.

What is a CRA self-assessment?

A CRA self-assessment is a document that summarizes a bank’s performance under the Community Reinvestment Act regulation during a specific time period. Performance is measured over a span of an exam cycle, which is typically 2–3 years. The document highlights key programs, retail distribution of products and services, and lending, service, and investment performance in the communities in which the bank serves. Basically, self-assessments support you in positioning and defending your CRA performance.

Why it’s important to conduct a CRA self-assessment

Conducting a CRA self-assessment ensures that you’re prepared to report your CRA progress to examiners. If you don’t put the work in upfront, you’re leaving it up to your examiners to figure out what your bank has done for its community. Examiners have limited time and resources to consider your bank’s performance in the community, and having a self-assessment will help you get the credit you deserve.

You know your CRA program best: the communities you serve, their challenges, their credit needs, and the impact your CRA program has forged over the past few years. A CRA self-assessment is your opportunity to tell your bank’s CRA story. This gives you, your bank’s leadership team, and your CRA examiners confidence that your bank is on track for the CRA rating that you know your bank deserves (Outstanding, anyone?).

A CRA self-assessment may be the most important tool you have in your CRA toolbox, and it keeps you ahead of examiners during an exam. It gives you a good idea of where you may have gaps in your performance, and it can help you better understand your bank’s demographic profile and how your bank’s products meet the needs of the community. It’s a living document you can use to strengthen your program by identifying areas of potential weakness ahead of time to share internally and strategize solutions to push your performance to the next level.

Although no agency requires a CRA self-assessment, the FDIC recommends performing CRA self-assessments to “review adequacy of Assessment Area, review your bank’s data, review your competitor’s data, and track progress.” Learn more about what the FDIC recommends here: The Community Reinvestment Act.

Where should you start?

Simply put, you should start where your CRA examiner starts.

An examiner will start by looking at your bank’s past Performance Evaluations and any notes they may have made during your last exam. This means you should get very familiar with your past Performance Evaluations prior to beginning your CRA self-assessment. Pay close attention to what your examiners looked at and commented on during the last exam.

Now it’s time to collect internal and external data, such as:

-

Your bank’s lending, service, and investment performance (think community development loans, investments, and service hours)

-

Internal strategies and CRA plans

-

HMDA data

-

Performance Evaluations of peer banks

-

National statistics

Then, refresh yourself on your regulator’s exam processes and protocols. You can find links to each regulator's exam processes here.

All this research will help you analyze your bank’s CRA program and prepare a solid self-assessment. It’s important to be familiar with how your bank and others have performed in the past and the current regulations because this should guide your future CRA program and your self-assessment.

What should your CRA self-assessment look like?

Since you aren’t required to create CRA self-assessments, there is no one best format. However, there are three general types of self-assessments that banks tend to create. Banks tend to create either a “lite” version that gets straight to the point, a “targeted” version focusing on an in-depth key performance metric, or a “comprehensive” analysis of a bank’s CRA program.

There is no right or wrong type of CRA self-assessment; it all depends on bank strategy, CRA leadership cycle, and program maturity. Remember to keep your self-assessment as relevant and concise as you can, and avoid adding information that examiners could find by doing a simple Google search of your bank.

Lite self-assessment

A lite self-assessment can be as simple as a 1–3 page executive-level assessment highlighting key programs and the top 2–4 performance elements you’re proud of. A lite self-assessment is useful for new CRA Officers or banks without an existing self-assessment. It provides a high-level view of your program to guide your CRA examiners.

Targeted self-assessment

If you know of performance gaps in your CRA program, a targeted self-assessment can help take control of your CRA story and guide how you address these gaps. Include performance tables and analysis in your performance context to show that you have identified weak spots and have a plan to move forward. It’s important to give examiners confidence in your CRA program, and you can do this by being proactive in identifying and sharing how you are moving forward.

Comprehensive self-assessment

A comprehensive self-assessment is ideal for more mature CRA programs with dedicated and experienced CRA professionals. In this type of assessment, you’ll look at everything your CRA examiner will look at. It’s an opportunity to showcase your performance, provide performance context to address gaps, and highlight your bank’s response.

Next steps

Preparing a self-assessment takes time, but the time invested yields a healthy return. When you put time into a CRA self-assessment, you’re telling your examiners, “We are confident and proactive. We know our communities. We run a professional CRA program, and we have a presumptive rating in mind.”

The benefits of conducting a CRA self-assessment don’t stop at your CRA exam. While the CRA self-assessment is ultimately for examiners and should be written for that audience, your bank may decide to create different versions of your self-assessment for your board, CRA committee, senior leadership, or key business units. This will help you share progress and build a culture of compliance at your bank. Use your findings to mature and improve your CRA program over time.

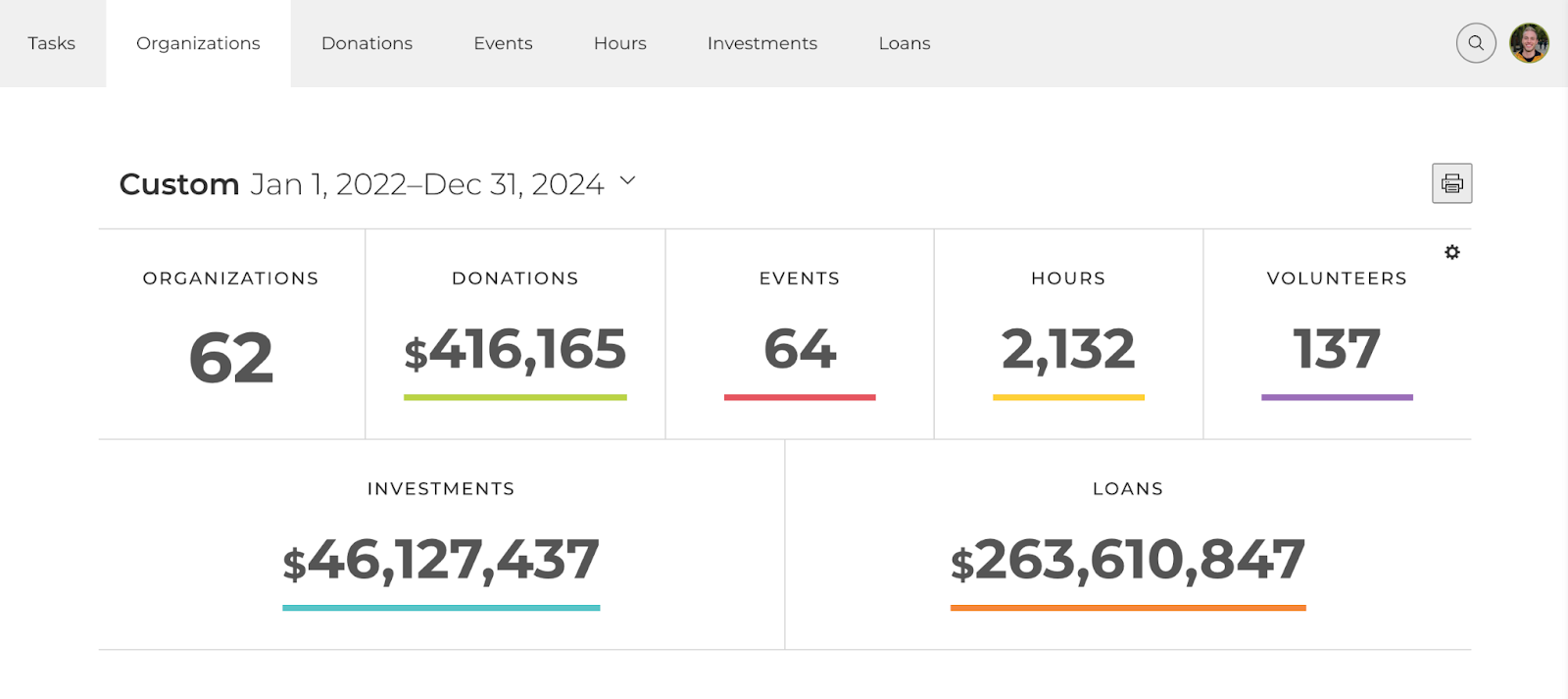

Track your data with Kadince software

In order to conduct a self-assessment, you’ll need easy access to your bank’s CRA data. This is much easier when all of your data is kept in one place, rather than in several different spreadsheets or binders.

Kadince software makes it easy to collect, track, and report your bank’s CRA data, including community development loans, services, investments, and more. When everything is kept in one place, you can easily conduct a CRA self-assessment with all the data you need. No more switching between spreadsheets and binders to find what you’re looking for. And when it’s time for your exam, you can give CRA examiners limited, read-only access to your Kadince account showing only the data you want them to see. It’s much easier to achieve your presumptive rating when everything examiners need is easily accessible.

Schedule a demo to learn how Kadince can help you collect and report the data you need to conduct an excellent CRA self-assessment!

None of Kadince, Inc., its affiliates, or its respective employees, directors, officers, and agents (collectively, “Kadince”) are responsible or liable for any content or information incorporated herein. Read full disclosure.

.png)